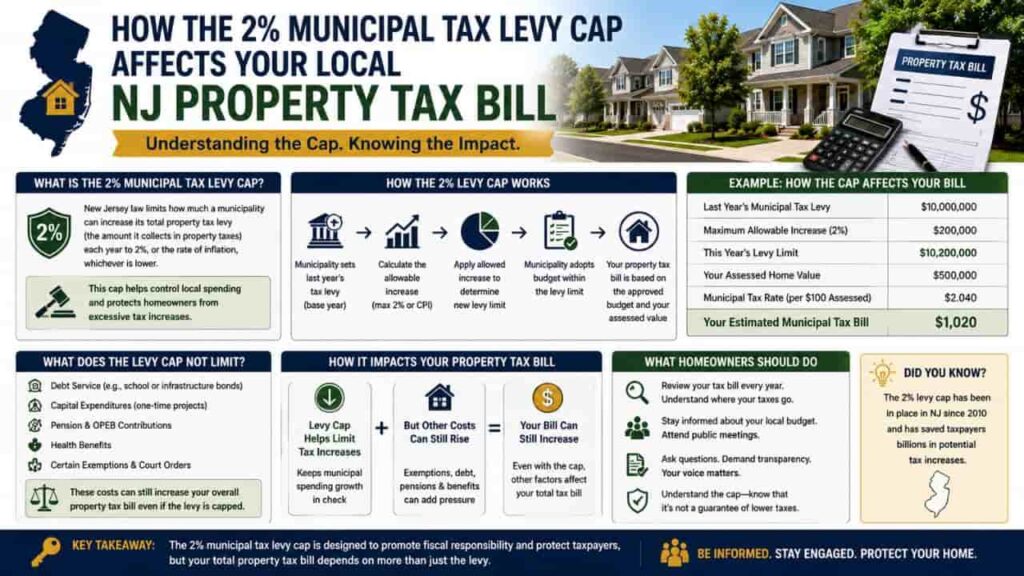

It is one of the most frustrating experiences for a New Jersey homeowner. You open your annual property tax bill expecting a modest change, only to find your total liability has jumped by 12%, 15%, or even 20%. Instantly, confusion sets in, Doesn’t New Jersey have a strict 2% property tax cap law? How is a double digit increase even legally possible? This disconnect stems from a widespread misunderstanding of how local fiscal policies operate under the Garden State’s statutory framework. The New Jersey 2 percent tax levy cap (enacted via Senate Bill S-2) is highly real, but it does not work the way most taxpayers think. It is a macro level restriction on local government budgets, not a protective micro cap on your individual residential tax assessment. This comprehensive guide breaks down the structural mechanics of the 2% cap, details the specific statutory exceptions that drive up costs, and explains how local structural shifts redistribute the tax burden directly onto your bill.

The Core Concept, Budget Levy Cap vs Individual Tax Bill

To understand why did my NJ property tax go up, you must first understand the fundamental difference between a tax levy and a tax assessment. The tax levy is the total aggregate dollar amount that a specific taxing district (like your municipality, school board, or county) is legally authorized to collect from all property owners combined to fund its annual operational budget. The tax assessment is the local tax assessor’s valuation of your individual parcel of real estate relative to the rest of the town.

The Golden Rule of NJ Property Tax. New Jersey has absolutely no cap on individual property tax bill increases or assessment growth. The 2% statutory cap applies strictly to the annual growth of the aggregate municipal tax levy.

If a town collected $10 million in total property taxes last year, the 2% cap means they can only collect $10.2 million this year for municipal purposes. However, how that total pool of $10.2 million is carved up and extracted from individual neighborhoods shifts every single year based on market data, physical home improvements and district revaluations.

The Three Components of Your New Jersey Tax Bill

Your final property tax bill is not a single, unified charge from your local township. Instead, it is a combined invoice reflecting three completely separate government entities, each operating under its own distinct fiscal constraints and budget cap calculations.

- The Municipal Portion (Capped at 2% with exemptions). Funds local services like police, public works, and administration.

- The Local School District Portion (Capped at 2% via separate rules). Funds public schools. This often consumes $50\%$ to $65\%$ of your entire annual property tax bill.

- The County Portion (Capped at 2% via county rules). Funds regional infrastructure, county courts, and county wide services.

Because these three budgets are calculated independently, a flat municipal budget can easily be completely overwhelmed by a sharp increase in the local school board or county infrastructure tax levy.

New Jersey 2 Percent Tax Levy Cap Exceptions

If all three government budgets face a structural 2% levy cap, how do overall town budgets still manage to outpace that number? The answer lies in the statutory New Jersey 2 percent tax levy cap exceptions written directly into N.J.S.A. 40A:4-45.45.

The state legislature recognized that certain local government expenses are completely uncontrollable. Therefore, the law allows taxing districts to automatically bypass the 2% limit for specific, high cost line items.

Statutory Cap Exclusions and Banking Provisions

- Debt Service Obligations.

Any funding required to pay off principal and interest on municipal bonds issued for long term capital infrastructure projects is completely unlimited and excluded from the cap. - Emergency Appropriations.

Extraordinary expenses tied to declared gubernatorial emergencies such as severe weather response, infrastructure failures, or catastrophic events can be added directly to the tax levy. - Pension and Healthcare Cost Surges.

If the cost of funding state mandated public employee pensions or state health benefits increases by more than 2%, the excess cost is exempted. - The Three Year Banking Provision.

If a municipality or school board increases its levy by less than 2% in a given fiscal year, it is legally permitted to “bank” that unused taxing capacity. This banked capacity can be deployed at any point over the next three succeeding budget years, paving the way for sudden, compounding tax increases down the line.

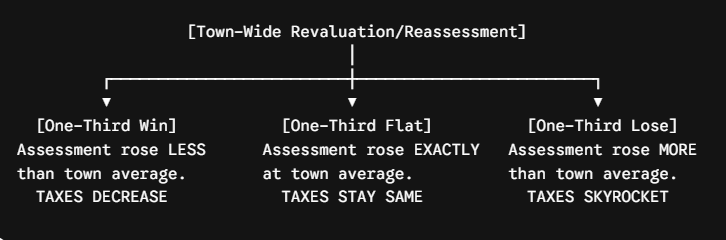

Municipal Revaluation vs. Reassessment, The Great Redistribution

The single biggest driver of massive, sudden spikes in an individual property tax bill is a structural town wide adjustment. This is where reassessment redistribution takes effect.

Even if a town obeys the 2% cap perfectly and does not increase its total budget by a single dollar, your personal tax bill can still skyrocket by 30% or more if your home’s value has grown faster than the town wide average.

| Operational Attribute | Municipal Revaluation | Municipal Reassessment |

| Trigger Mechanism | Typically court ordered or directed by the State Division of Taxation due to inequitable ratios. | Undertaken voluntarily by the local tax assessor and approved by the County Board. |

| Physical Scope | Requires a full interior and exterior physical inspection of every parcel by an outside firm. | Uses existing property records, desktop valuations, and targeted exterior inspections. |

| Tax Filing Deadline Change | Extends the standard statutory tax appeal filing deadline from April 1 to May 1. | Extends the standard statutory tax appeal filing deadline from April 1 to May 1. |

The “One Third” Rule of Revaluations

When a town wide revaluation or reassessment maps all properties to 100% of their true market value, the total tax burden is completely shifted across the population. As a general rule of thumb, the outcome splits the town into three distinct categories.

If your neighborhood experienced rapid real estate appreciation while the rest of the municipality lagged behind, a revaluation will force you to absorb a much larger slice of the total tax pie. This is why your tax bill can increase dramatically despite macro level budget caps.

Actionable Steps for New Jersey Homeowners

If you find yourself on the losing side of a reassessment redistribution, you are not entirely powerless. You can actively take steps to audit your liability and protect your finances.

Step 1. Review Your Property Record Card

Visit your municipal tax assessor’s office and request your official property record card. Check the structural data for simple data errors. If the town erroneously believes your home features a finished basement, four bedrooms instead of three, or more livable square footage than actually exists, your baseline assessment is artificially inflated.

Step 2. Track Your Local Budget Hearings

School boards and municipal councils are legally required to hold public budget hearings before finalizing their tax levies. Attend these sessions to monitor how much banked cap capacity they intend to deploy and check whether they are maximizing their statutory exceptions for debt service or healthcare allocations.

Step 3. File an Annual Assessment Appeal

If the local assessor’s determination of your home’s true market value exceeds actual closed comparable sales in your immediate neighborhood from the prior pre tax year, file a formal appeal with your County Board of Taxation before the strict April 1 deadline (or May 1 if your town completed a revaluation).

Conclusion

Understanding how much can property taxes increase in NJ annually requires looking beyond the widely discussed 2% tax levy cap. While Senate Bill S-2 successfully prevents local government budgets from expanding completely out of control, it offers no individual protection during a municipal revaluation vs reassessment cycle. Your local property tax bill is ultimately a reflection of your shifting share of the local real estate market. By staying informed on local municipal exceptions, analyzing neighborhood sales data, and auditing your property record card, you can successfully understand the complexities of New Jersey’s property tax structure.

FAQs

How much can property taxes increase in NJ annually?

There is no maximum legal limit on how much an individual property tax bill can increase. The state’s strict 2% cap applies only to the total aggregate budget levy raised by the municipality.

Why did my NJ property tax go up if there is a 2% cap?

Your bill likely increased due to a town wide revaluation shifting the tax burden to your neighborhood, or because your local school, county, or municipal budgets triggered allowed statutory cap exceptions.

What are the main New Jersey 2 percent tax levy cap exceptions?

The primary legal exclusions include annual debt service payments, extraordinary costs from declared weather emergencies, pension contribution increases, and public employee healthcare cost spikes exceeding 2%.

What is the difference between a municipal revaluation vs reassessment?

A revaluation is a comprehensive, often court ordered program requiring physical interior and exterior inspections of all homes by an outside firm. Reassessments are done internally by local assessors using statistical market updates.

Does the 2% tax levy cap apply to local school districts?

Yes. School districts face a separate 2% cap on their general fund tax levy, but they can exceed it via specific state waivers for enrollment changes or through a public voter referendum.

What is a reassessment redistribution in New Jersey real estate?

It is the structural reallocation of the town’s tax burden. If a revaluation reveals your home’s value grew faster than the municipal average, your tax bill will rise to reflect your larger market share.

Can a town increase its tax levy by more than 2% without exceptions?

Yes, but only if they have “banked” unused cap room from the prior three years, or if they successfully pass a local public budget referendum with a majority vote from residents.

Does a higher property assessment automatically mean higher taxes?

No. If everyone’s assessment doubles during a revaluation, the total tax rate drops proportionately. Your taxes only increase if your assessment grows at a higher rate than the town average.

Does a town revaluation extend the property tax appeal deadline?

Yes. In a standard year, the statutory tax appeal deadline is April 1. If your municipality implements a town wide revaluation or reassessment, the filing deadline is legally extended to May 1.

How can I lower my bill if my assessment outpaces the 2% cap?

You must file a formal tax appeal with the County Board of Taxation by the legal deadline, providing concrete evidence that your assessed value exceeds your home’s actual true market value.