Every year, thousands of New Jersey homeowners discover that their property tax assessments do not accurately reflect the actual market value of their homes. Because New Jersey consistently ranks among the highest states for property tax burdens, ensuring your assessment is accurate is critical. If your property is overassessed, you are paying more than your fair share. This comprehensive, step by step guide explains how to manage the New Jersey property tax appeal process in 2026, utilizing official statutory frameworks, structural real estate data, and proven valuation methodologies to help you successfully lower your tax burden.

Understanding the Foundation of NJ Property Tax Assessments

To build a winning appeal, you must first understand that you cannot appeal the total tax dollar amount or the tax rate itself. Instead, you must appeal the assessment of your property’s value. The local tax assessor determines your property’s assessed value as of October 1 of the pre tax year (known as the statutory valuation date). This assessment is supposed to reflect the true market value of your property, or a percentage of it adjusted by the municipality’s specific equalization parameters.

The Role of the Chapter 123 Ratio

New Jersey utilizes a unique mechanism known as Chapter 123 (N.J.S.A. 54:1-35a) to determine if an assessment is fair. Municipalities do not always assess properties at $100\%$ of true market value; instead, they operate at an “average ratio” established by the State Division of Taxation. The Chapter 123 ratio creates a “common level range” (typically 15% above or below the average ratio). If your property’s assessment-to-market-value ratio falls outside this corridor, the County Board of Taxation will adjust your assessment to the common level.

Missing the Date Means Forfeiting Your Right to Appeal

The New Jersey tax appeal timeline is strictly enforced by state law. Failing to file your petition on time will result in an automatic dismissal of your case, with no room for extensions.

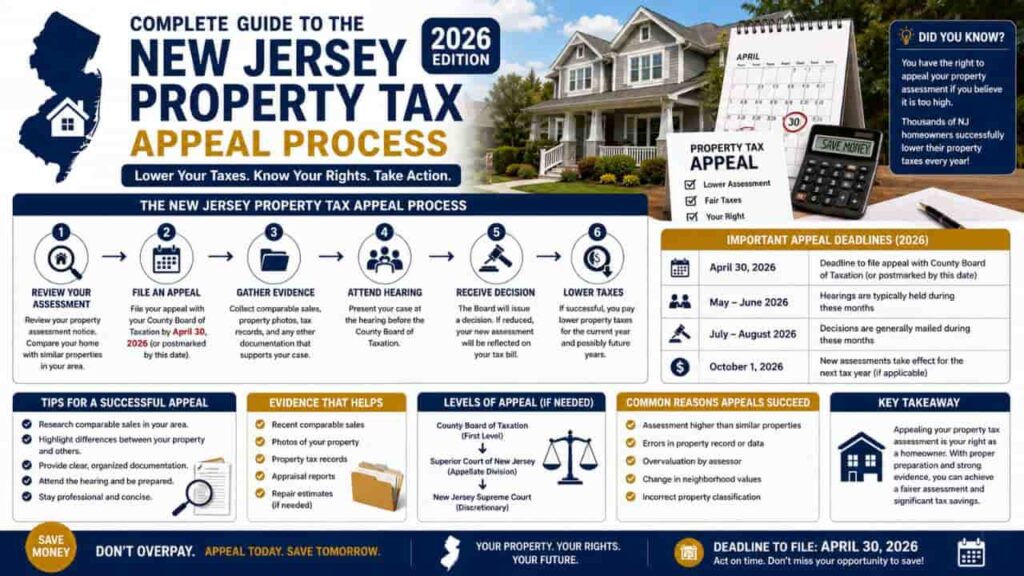

2026 Key Filing Deadlines

- April 1, 2026. This is the standard deadline for most New Jersey municipalities. Your petition must be received (not postmarked) by the County Board of Taxation and the municipal clerk by this date.

- May 1, 2026. This extended deadline applies exclusively to residents living in municipalities undergoing a district wide reassessment or a complete structural revaluation.

| Assessment Event Type | Official Filing Deadline | Required Receiving Entities |

| Standard Municipal Assessment | April 1, 2026 | County Board of Taxation & Municipal Clerk |

| Revaluation / Reassessment | May 1, 2026 | County Board of Taxation & Municipal Clerk |

| Worldwide/State Disaster Extension | Determined by Executive Order | State Tax Court / County Board |

Step by Step Guide, How to Appeal Property Tax in NJ

Managing the logistical pipeline requires precision. Follow these structural steps to ensure your appeal is legally valid and structurally sound.

Step 1. Review Your Chapter 75 Card

In February, you should have received a green Chapter 75 Assessment Notice Card. This document lists your current land assessment, structural improvements value, total taxable valuation, and the prior year’s taxes. Verify these numbers immediately.

Step 2. Determine Where to File Based on Valuation

The jurisdiction of your appeal is dictated by the total assessed value of your property.

- Assessed Value of $1,000,000 or Less.

You must file your initial appeal with your local County Board of Taxation using a standard Petition of Appeal form. - Assessed Value Exceeding $1,000,000.

You have the legal right to bypass the County Board completely and file a direct appeal with the Tax Court of New Jersey using NJ Tax Court Appeal Form A-1.

Step 3. Gather Structural Data and Comparable Sales (Comps)

Your appeal will stand or fall based on objective real estate market data. To prove your home value is overassessed, you must present evidence of comparable sales (Comps) that occurred prior to October 1 of the pre tax year.

Expert Insight. Assessment appeals are won by proving market value, not by comparing your taxes to your neighbor’s taxes. You must present actual, closed real estate transactions of similar properties in your immediate neighborhood.

Proving Overassessment Using Structural Data and Comps

To build an airtight evidentiary package for the County Board of Taxation or the New Jersey Tax Court, your comparable sales must meet strict legal and structural criteria.

Guidelines for Selecting Valid Comparable Sales

- Proximity and Neighborhood. Select homes within your immediate subdivision or within a one-mile radius if you are in a suburban township.

- Style and Architecture. Compare apples to apples. If you own a ranch style home, do not use a multi-story colonial as a comp.

- Timeframe Constraint. Comps must be valid sales that closed before October 1, 2025 (for the 2026 tax year). Post October sales are generally inadmissible as primary evidence.

- Transaction Validity. Avoid “non arms length” transactions. Foreclosures, short sales, estate sales, and transfers between family members do not represent true market value and will be disqualified by the municipal attorney.

Structural Adjustments to Look For

When analyzing your properties against the comps, document significant structural variances that detract from your property’s value relative to the market.

- Square Footage Differential. Substantial differences in living space.

- Functional Obsolescence. Outdated layouts, lack of a garage, or unique structural defects.

- Environmental Subjection. Proximity to major highways, high voltage power lines, commercial zoning, or location within a designated flood plain.

Navigating the County Board of Taxation Hearing

Once your petition is filed and the standard fees are paid, you will receive a notice for a formal hearing. Treat this hearing with the same preparation you would bring to a court of law.

Evidence Exchange Rule

You must supply a copy of your comparable sales analysis to the tax assessor and the County Board of Taxation at least seven calendar days prior to your scheduled hearing. If you fail to do this, your evidence will be excluded.

What Happens During the Hearing?

The hearing is structured to move quickly. The petitioner (the homeowner) presents their case first, detailing the comparable sales and explaining why the assessment exceeds true market value. Next, the municipal tax assessor or municipal attorney cross examines your data and presents their own supporting comps. The Board commissioners will review the evidence, apply the Chapter 123 ratio parameters, and issue a formal written judgment (usually a Judgment Code 2B for a reduction, or a Code 2A if the assessment is affirmed) within a few weeks.

Summary Checklist for a Successful 2026 Appeal

- Checked the Chapter 75 card for accuracy.

- Determined the proper filing track (County Board vs. Tax Court Form A-1).

- Sourced 3 to 5 valid, arm’s length comparable sales closing before October 1, 2025.

- Calculated the Chapter 123 ratio to verify true value deviation.

- Filed the petition prior to the April 1 / May 1 deadline.

- Served copies of the evidence packet to the municipal assessor 7 days before the hearing.

Conclusion

Mastering the New Jersey property tax appeal process 2026 requires strict compliance with statutory timeline frameworks and accurate evaluation methodologies. Successfully proving that your home value is overassessed hinges on presenting verified, arm’s length comparable sales (Comps) before the rigid legal deadlines. By understanding the structural mechanics of the County Board of Taxation and leveraging statutory tools like the NJ tax court appeal Form A-1, New Jersey homeowners can confidently challenge unfair assessments, navigate valuation hearings, and secure long term property tax relief.

FAQs

How to appeal property tax in NJ 2026?

File a formal petition with your County Board of Taxation by the statutory deadline, providing 3 to 5 verified comparable sales proving your assessment exceeds true market value.

What is the New Jersey tax assessment appeal deadline for 2026?

The standard official deadline is April 1, 2026. However, if your municipality underwent a district wide property revaluation or structural reassessment, the extended deadline is May 1, 2026.

When should I use NJ tax court appeal Form A-1?

Use Form A-1 to file a direct appeal with the Tax Court of New Jersey if your property’s total assessed valuation exceeds the $1,000,000 legal threshold.

What is the Chapter 123 ratio in NJ property tax appeals?

It is a statutory formula used by the state to test assessment fairness. If your assessment to market value ratio deviates from this common level range, your assessment gets adjusted.

Can I appeal my actual property tax dollar amount or tax rate?

No. By law, you can only appeal the structural assessed value of your property determined by the tax assessor. You cannot appeal local tax rates or budget allocations.

What qualifies as a valid comparable sale (Comp) for an appeal?

Valid comps must be local, structurally similar, arm’s length market transactions that legally closed before the October 1 statutory valuation date of the preceding pre tax year.

What is a non arms length transaction in real estate data?

These are sales involving foreclosures, short sales, estate liquidations, or transfers between family members. They do not represent fair market value and are disqualified during hearings.

What is the 7 day evidence exchange rule in New Jersey?

Homeowners must legally deliver their entire comparable sales analysis evidence packet to the local municipal tax assessor and County Board at least 7 calendar days before the hearing.

What happens if I miss the NJ property tax appeal deadline?

New Jersey statutory tax deadlines are strictly enforced. Missing the April 1 or May 1 filing date results in an automatic, non negotiable dismissal of your assessment appeal case.

Do I need an attorney for a County Board of Taxation hearing?

Individual homeowners are legally permitted to represent themselves at County Board hearings. However, corporations or entities filing appeals must be represented by a licensed New Jersey attorney.